.png)

Are you dreaming of building a custom home in Oklahoma but feel overwhelmed by the financing? You're not alone. The journey from a patch of land to your dream front door can feel complex, especially when a traditional mortgage won't cover it. This is where construction loans in Oklahoma become the key to unlocking your vision.

Imagine this loan as the financial blueprint for your future home. It’s designed specifically for new builds, releasing funds in stages as your home in Edmond, Moore, or even a rural retreat in Macomb takes shape. At ACET Custom Homes, we’ve spent over 15 years guiding families through this exact process, turning financial hurdles into stepping stones. As one of our recent clients shared, "The team at ACET made a complex process feel manageable and were with us every step of the way." That’s our promise: clarity and confidence from day one.

How Construction Loans Fund Your Oklahoma Dream Home

Think of it this way: you wouldn't get a car loan for a vehicle that’s still a pile of parts. The same logic applies here. A standard mortgage is for an existing house, but a construction loan is the specialized tool you need to build from the ground up.

This short-term loan is crafted to cover every cost, from buying your lot and preparing Oklahoma’s unique clay soil to pouring the foundation and installing those perfect final finishes. It provides the lifeblood for your project, ensuring a steady flow of funds to keep everything moving.

How Does It Actually Work? The Draw Process

Unlike a traditional mortgage where you get a lump sum at closing, a construction loan pays out in stages called "draws." Each draw corresponds to a specific, completed milestone in the building process.

This phased approach protects both you and the lender by ensuring money is only paid for work that’s actually been completed and verified. It’s a system built on accountability.

What a Typical Draw Schedule Looks Like

Here is a step-by-step breakdown of a common draw schedule:

- Initial Draw: Covers the land purchase (if not already owned), permits, and initial site work.

- Foundation Draw: Released once the slab is poured, cured, and passes inspection.

- Framing Draw: Paid out after the home's structural skeleton is complete.

- "Dry-In" Draw: Disbursed when the roof, windows, and exterior doors are installed, protecting the home from Oklahoma weather.

- Final Draws: Cover interior work like drywall, plumbing, electrical, flooring, and final finishes.

For a deeper dive into local lenders, check out our guide on the best mortgage companies in Oklahoma City.

Construction Loan vs. Traditional Mortgage: A Quick Comparison

Understanding the key differences is crucial. While both get you into a home, their purpose and structure are fundamentally different.

Knowing these distinctions is the first step toward building a solid financial foundation for your custom home project.

Choosing the Right Type of Construction Loan

When you start exploring construction loans in Oklahoma, you’ll find it’s not a one-size-fits-all situation. The right loan depends on your project, finances, and how much complexity you’re willing to manage.

Think of it like choosing a vacation. Do you want an all-inclusive resort where everything is handled, or do you prefer to book each component separately for more flexibility? Both work, but they offer very different experiences.

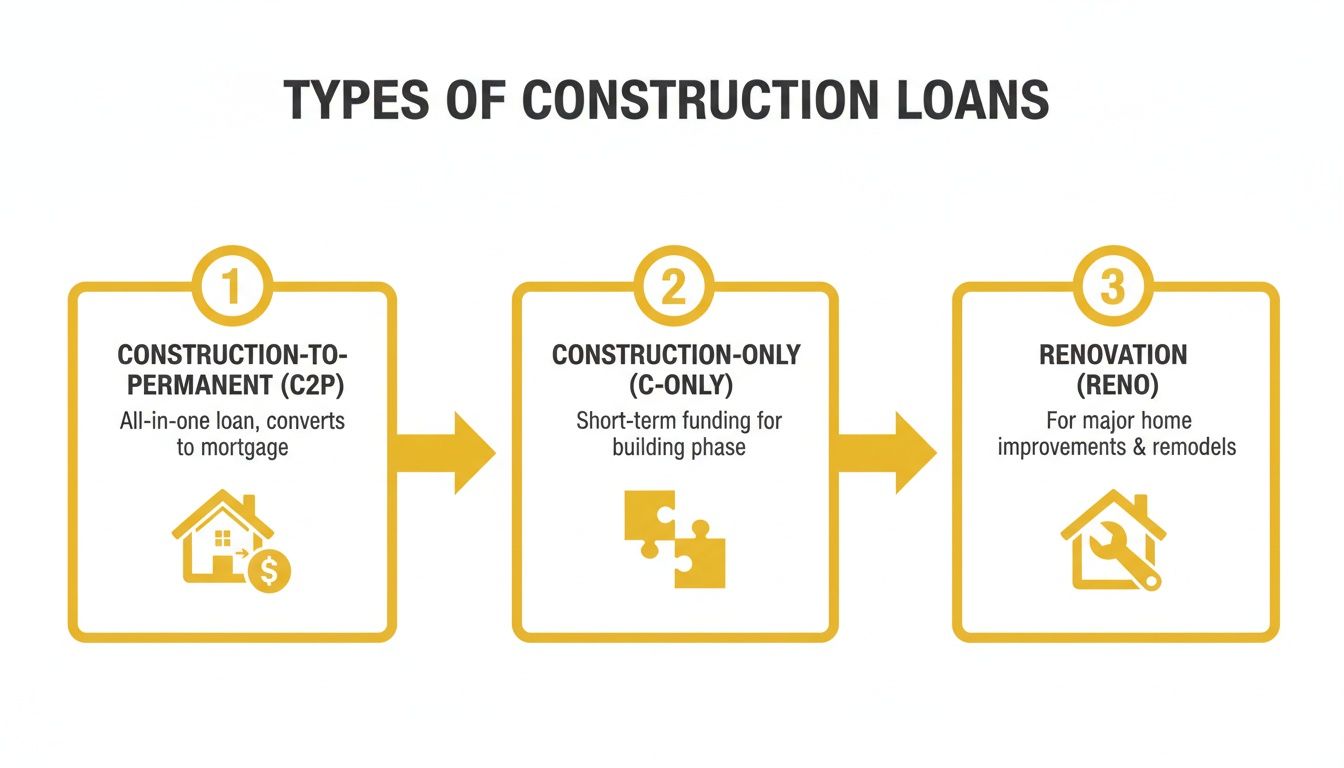

The All-Inclusive Path: Construction-to-Permanent Loans

For most people building a custom home in Oklahoma, from OKC to rural Guthrie, the Construction-to-Permanent (C2P) loan is the best choice. Often called a “one-time close” loan, it combines the construction financing and your final mortgage into a single, seamless package.

You go through one application, one underwriting process, and one closing. During the 12- to 18-month construction phase, you only pay interest on the money your builder has used. Once your home is complete, the loan automatically converts into a standard 15 or 30-year mortgage. No more paperwork, no more closing costs. This simplicity is a massive relief during an already busy process.

The A La Carte Method: Construction-Only Loans

A Construction-Only loan is your "a la carte" option. This loan provides funds only for the building phase. As soon as the home is finished, the entire loan becomes due.

To pay it off, you must secure a second, separate mortgage—a “two-time close.” This means two applications, two credit checks, and two sets of closing costs. Why choose this? Flexibility. If you believe interest rates will drop or your credit score will improve by the time your home is built, you could potentially secure a better rate. However, it’s a gamble. If market conditions worsen, you could be left scrambling for financing.

Upgrading an Existing Home: Renovation Loans

What if your dream home is the one you’re already in, but it needs a major facelift? A Renovation Loan is designed for this. It bundles the cost of a major remodel or addition with your current mortgage.

This is a fantastic option if you’ve found a house with great bones in a perfect location like Deer Creek but want to add a second story or completely gut the kitchen. For a more detailed look, our article on the various aspects of Oklahoma construction loans breaks it down even further.

Working with an experienced team is non-negotiable. As the Federal Deposit Insurance Corporation (FDIC) reported, construction loan delinquency rates can be volatile, underscoring the need for a solid, trusted team to navigate any market conditions.

Your Step-by-Step Guide to the Loan Process

Securing financing for your custom home in Oklahoma might seem daunting, but it’s just a series of manageable steps. When you know the roadmap, the journey becomes clear and straightforward.

Let's walk through the process, from initial budgeting to breaking ground.

Stage 1: The Initial Game Plan and Budgeting

Before talking to a bank, you need a realistic grasp of your budget. This involves a hard look at your savings, income, and financial obligations to determine what you can comfortably afford. We often sit down with clients to map out a preliminary budget that includes land, design, materials, and a contingency fund for unexpected costs.

Stage 2: Getting Pre-Approved by a Lender

Next, get pre-approved by a lender who specializes in construction loans in Oklahoma. This conditional approval from the bank tells you exactly how much you can borrow and serves as a crucial reality check.

Be ready to provide:

- Proof of Income: W-2s, pay stubs, and recent tax returns.

- Asset Verification: Bank and investment account statements.

- Debt Overview: A list of car loans, student loans, or credit card balances.

- Credit Check: The lender will pull your credit report.

Stage 3: Choosing Your Builder and Finalizing Plans

This is one of the most critical decisions you'll make. Lenders require a reputable, licensed, and insured builder with a solid track record. Knowing the crucial questions to ask a general contractor is a smart first step.

At ACET Custom Homes, our 15+ years of experience and strong relationships with Oklahoma lenders help streamline this process. Once you’ve chosen your builder, you’ll finalize the architectural plans and a detailed "spec sheet" listing every material and finish. Learn more about our custom home building process.

Stage 4: The Appraisal and Full Loan Submission

The lender will order an appraisal based on the future value of your home once it's built, using your finalized plans. The appraiser considers the location—whether a prime lot in Edmond or acreage near Shawnee—and comparable new homes to determine the "as-completed" value. This appraisal, along with your builder's contract and budget, forms the complete loan package.

The infographic below shows the different types of loans you might be considering.

As you can see, the single-close, construction-to-permanent loan is often the most direct route for building a custom home.

Stage 5: Underwriting and Closing the Deal

Underwriting is the final checkpoint. The lender’s team will re-verify your credit, employment, and all project details. Once the underwriter gives the final approval, you’ll head to the closing table to sign the official loan documents. The moment the ink is dry, the initial draw is funded, and your builder can finally break ground.

Understanding the Costs of Your Oklahoma Build

Let's talk numbers. A firm grip on the financial side of construction loans in Oklahoma is essential to keep your project on track and stress-free. It’s about understanding every cost, from the down payment to the final interest charge.

A well-planned budget is the true foundation of a successful custom home, whether you’re building in Deer Creek or out near Shawnee.

The Down Payment: What to Expect

Lenders in Oklahoma typically require a higher down payment for construction loans, usually 20% to 25% of the total project cost, due to the increased risk.

Good news: if you already own your land, you can often use its equity to cover some or all of the down payment. This can significantly reduce the cash you need to bring to the table.

Interest Rates and Closing Costs

During the build, you’ll typically pay interest only on the money that has been released to your builder. These construction-phase loans often have a variable interest rate.

Don’t forget to budget for closing costs, which include:

- Appraisal Fees: To determine the home's future value based on your plans.

- Origination Fees: The lender's fee for processing the loan.

- Title Insurance: Protects you and the bank from claims against the property title.

- Inspection Fees: To verify work is complete before each draw is released.

The Draw Schedule: Your Project's Financial Heartbeat

The draw schedule is a critical part of your loan agreement. It's a payment timeline that dictates when your lender gives money to the builder based on completing specific construction milestones.

"A well-structured draw schedule protects both the homeowner and the builder, ensuring funds are aligned with tangible progress on site. It’s all about transparency and accountability."

— Bono, Project Manager at ACET Custom Homes

A typical draw schedule breaks down like this:

- Initial Draw: Covers the land purchase, permits, and site preparation. Understanding site preparation excavation helps in budgeting for this foundational expense.

- Foundation Poured: The next draw is released once the concrete slab is in and cured.

- Framing Complete: Payment is made after the home's skeleton is standing.

- Dry-In Stage: Funds are released when the roof, windows, and exterior doors are installed.

- Final Draws: Cover interior work, finishing touches, and final inspections.

This system keeps your project moving smoothly. To see how these costs fit into the bigger picture, check out our guide on luxury home construction costs.

Navigating Oklahoma-Specific Building Challenges

Building a custom home in Oklahoma comes with unique challenges, from our expansive clay soil to severe weather. Lenders know these risks and want to see that your builder has a plan to address them. A proactive approach shows your project is a solid investment, not a gamble.

At ACET Custom Homes, our 15+ years of local experience mean we anticipate these issues, giving lenders the confidence they need to approve your financing.

Tackling Oklahoma's Expansive Clay Soil

Much of Oklahoma, especially around the OKC metro, has expansive clay soil. This soil swells when wet and shrinks when dry, which can wreak havoc on a standard foundation.

Lenders scrutinize foundation plans for this reason. An experienced builder like ACET Custom Homes will work with engineers to design specialized foundations, such as post-tension slabs, engineered to withstand this movement. Presenting these plans adds serious credibility to your loan application.

Designing for Weather and Energy Efficiency

Oklahoma's weather is no joke. Tornadoes and high winds mean our building codes are stringent. Lenders and insurers require homes to meet or exceed these standards with features like reinforced framing and storm shelters.

Additionally, our hot summers and cold winters make energy efficiency crucial. Lenders favor plans that include high-performance insulation, quality windows, and effective moisture management systems. Highlighting these features demonstrates you're building a high-quality, cost-efficient home. Understanding how a proper moisture barrier works is a key part of this.

Economic Factors in Oklahoma Construction

The local economy influences the lending climate. While construction is a major part of Oklahoma's GDP, it's not immune to market swings. A recent Oklahoma Economic Indicators report noted a contraction in residential investment due to shifting mortgage rates. For a luxury builder like ACET Custom Homes, this highlights the importance of working with professionals who can navigate these shifts confidently.

Ultimately, getting your loan approved is about showing you've considered every variable. A plan that addresses Oklahoma's specific challenges—whether you're building in Moore or Chickasha—is a plan that gets funded.

Frequently Asked Questions About Construction Loans in Oklahoma

What credit score do I need for a construction loan?

Most Oklahoma lenders look for a FICO score of 700 or higher. A stronger score often leads to better interest rates and more favorable terms. If your score is slightly lower, some lenders may still work with you, especially if you have a larger down payment.

Can I use my land as a down payment?

Yes, absolutely! If you already own your lot, whether in a suburban neighborhood like Deer Creek or on acreage near Chickasha, you can use its equity toward your down payment. For example, if your land is valued at $100,000 and your required down payment is $100,000, you may not need to provide any additional cash.

How long does the loan approval process take?

Plan for the construction loan approval process to take between 45 and 90 days. This timeline accounts for gathering financial documents, finalizing home plans, the appraisal, and the lender's underwriting. An organized builder can help keep this process moving efficiently.

What happens if construction costs go over budget?

This is why a contingency fund is essential. Most lenders will require you to set aside 5% to 10% of the total construction cost as a buffer for unexpected expenses, like a sudden rise in material prices. At ACET Custom Homes, we create detailed budgets from the start and manage costs carefully to prevent overruns.

Ready to design your custom home? Schedule a free consultation with ACET Custom Homes today.

Consultation Today!